3 Year-End Tips to Get Ahead on Law Firm Taxes

12/04/2024 By Dan Bowman

The end of the year is always a busy time for law firms. Wrapping up cases, closing out finances, and planning for the new year can leave even the most organized teams feeling stretched thin. Among all the chaos, tax-related tasks often get pushed aside — sometimes until it’s too late to handle them effectively.

To avoid last-minute stress or unnecessary complications, it’s important to get ahead of these responsibilities. Here are three tax tips every law firm should prioritize before 2025.

Tip #1: Don’t Wait to Compile and Organize All Financial Documents

Keeping thorough and accurate records is a vital step for preparing taxes, and compiling them all together can be a time-consuming process. While the specifics depend on your firm’s structure and the work you’ve done this year, here are some common items to include:

- Income Records: Detailed records of all income sources, including client invoices, retainer fees, and any other revenue streams.

- Expense Documentation: Receipts and invoices for all business-related expenses, such as office supplies, travel, professional development, and client entertainment.

- Payroll Information: Comprehensive payroll records, including salaries, bonuses, benefits, and tax withholdings for all employees.

- Contractor Payments: Forms 1099-NEC for payments made to independent contractors exceeding $600.

- Bank Statements: Monthly statements for all business accounts, including operating, savings, and trust accounts.

- Trust Account Records: Detailed records of client trust accounts, ensuring compliance with state bar regulations.

- Asset Information: Documentation of business assets, including purchase dates, costs, and depreciation schedules.

- Loan Documents: Agreements and payment records for business loans or lines of credit.

- Tax Filings: Copies of previous years’ tax returns and any correspondence with tax authorities.

- Legal Documents: Records of any legal proceedings, settlements, or judgments involving the firm as a party.

- Insurance Policies: Details of business insurance coverage, including premiums paid.

- Retirement Plan Contributions: Records of contributions to employee retirement plans, such as 401(k) or SEP IRA accounts.

- Mileage Logs: If applicable, detailed logs of business-related vehicle use.

- Home Office Expenses: For attorneys claiming a home office deduction, records of expenses related to the portion of the home used exclusively for business.

For firms managing trust accounts, review these records carefully to confirm they’re accurate and in compliance with state bar regulations. Staying organized now means fewer surprises when your accountant starts preparing your return.

Tip #2: Settle Outstanding Invoices and Payables

Year-end taxes obviously involve what you’ve earned, but they’re also impacted by what’s owed to you and what you owe to others. Addressing both accounts receivable and accounts payable is important to wrapping up your firm’s financials responsibly.

Accounts Receivable

Reach out to clients with outstanding balances and aim to collect overdue payments before December 31. Not sure where to start? Prioritize clients with larger balances or those approaching 90 days past due. A simple email reminder or phone call often goes a long way. Make sure your invoices clearly outline the amount due and any applicable deadlines.

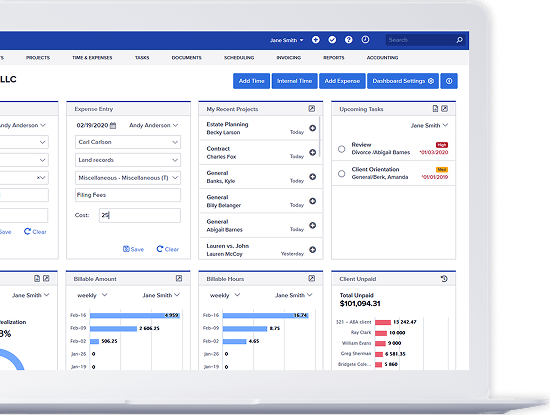

To make this process smoother, consider using software that automates payment reminders and offers clients easy online payment options. For example, the legal practice management software Bill4Time provides features that allow law firms to send automated invoice reminders and accept online payments, which can lead to faster collections.

Accounts Payable

If your firm operates on a cash basis for tax purposes, paying outstanding bills by the end of the year may help reduce your taxable income. Consider pre-paying recurring expenses like rent, utilities, or professional dues. Additionally, review whether you’ve accrued expenses that should be recorded, even if they haven’t been paid yet.

When you balance what’s coming in and what’s going out, you’ll have a clearer understanding of your firm’s financial health and position yourself to make smart tax decisions.

Tip #3: Meet with Your Accountant to Plan Strategically

An accountant is an essential partner in making sound financial decisions. Schedule a year-end consultation to discuss your firm’s finances, and go into the meeting prepared with detailed records and clear goals. Some questions you can ask your accountant include:

- Can we maximize deductions for 2024? Are there expenses we’ve overlooked or new deductions we qualify for?

- Should we make any major financial moves before December 31, like contributing to a retirement plan or purchasing office equipment?

- Are we on track with estimated tax payments?

- How will changes in tax laws impact our firm’s obligations for 2024 or 2025?

Preparing your documentation ahead of time allows your accountant to provide meaningful advice and reduces the risk of delays. Scheduling this meeting in early December or even November — before accountants get swamped with last-minute requests — can make the entire process less stressful.

Start Preparing Now for a Stress-Free Tax Season

Taking early steps to organize your firm’s financial records can make a big difference when tax season arrives. Sorting through paperwork, addressing unresolved financial matters, and working with your accountant ahead of time gives you a clearer view of what needs attention.

An organized approach is easier when you have tools designed to simplify the process. Legal practice management software like Bill4Time can help you stay on top of your firm’s financial data all year. By combining features like time tracking, billing, and case management in one system, it keeps everything accessible and accurate. When it’s time to prepare taxes, generating detailed reports and sharing them with your accountant becomes far less complicated.

Check it out for yourself! Click below to start a 7-day free trial.