Legal time tracking software is typically how lawyers calculate their billable hours and keep track of everything. According to the American Bar Association, nearly 9 out of 10 firms were already using time tracking software by 2021, and for multiple reasons. The complex nature of time tracking requires methods that keep lawyers organized and accurate — two goals time tracking software helps facilitate.

This software can be, for an attorney, like a “billable hours calculator” that works based on start-and-stop timers and custom hourly rates. This reduces potential errors and speeds up the billing process, as you track time in the same software that generates your invoices.

Finding the best legal time tracking software for your firm can make a world of difference in your efficiency, whether you’re a solo practitioner or running a large corporate practice. But with a ton of options on the market, it’s helpful to know what you’re looking for. Read on to learn more about effectively tracking time and how exactly time tracking software can work for your firm.

How to Keep Track of Billable Hours Effectively

Generally, there are two ways you can track time: manually and digitally. Let’s examine both.

Manual Tracking

Various methods of tracking by hand have emerged over the history of practicing law, all of which have their own pros and cons. Some of the most common methods include:

- Real-Time | Writing down time spent on tasks as they occur — for example, spending a half-hour answering a client’s email and then immediately writing down the time spent.

- Intervals | Rather than tracking things as they happen, attorneys may opt to do all of their tracking in regular intervals, typically daily or even weekly.

- Delegated | An attorney passes their entries to a paralegal or assistant, who enters the times into the firm’s tracking system of choice (e.g., spreadsheets, paper charts)

- Calendaring | Many attorneys will simply reference their calendars to calculate billable hours. Events, emails, meetings, and court dates are reference points for this method.

Manual tracking methods like the ones above come with several pros: they’re simple, easy to understand, and follow some sort of consistent timing that easily slots them into a routine. Essentially, they are a “quick and dirty” way to get a close estimate of billable hours.

Unfortunately, manual methods are often subject to human error — through flawed arithmetic, mistakes while entering data, or simply not being exact enough.

Sometimes, simply forgetting to bill for certain tasks can happen as well. Even the best attorneys with the sharpest memories might forget to bill for tasks, especially if there is a gap of time between completing tasks and recording them. Recent studies show that the Ebbinghaus Forgetting Curve theory still rings true today, which more or less means if you don’t write something down right away, you’re very likely to lose it!

Digital Tracking

While manual methods have been around for decades, software built specifically for tracking billable hours has become the preferred choice for many attorneys. Unlike spreadsheets, which were adapted for timekeeping but not designed for it, legal time tracking software allows lawyers to log their hours as they work, apply custom billing rates, and generate invoices with ease.

A recent TechReport by the American Bar Association highlighted a growing reliance on digital time tracking across the legal field:

- Roughly two-thirds (66%) of firms use time tracking software.

- Nearly 85% of lawyers reported personally using remote-access software.

- Seven out of 10 firms are using cloud-based software in their operations.

Additionally, there is a clear trend towards using digital tracking in favor of manual tracking, especially via cloud-based software. Solo lawyers, for example, nearly tripled their usage rate from the previous year.

Ultimately, while manual tracking methods have improved over the years, digital methods are quickly becoming the norm for practicing attorneys. Time tracking software is far easier to do in real time — regardless of where you are — which gives you an easy, efficient way to record your time right after completing a task.

Is There a Tool to Track Billable Hours for Different Practice Areas?

A high-quality legal time tracking software will have multiple ways to account for different practice areas. Some features that work great for unique situations in various practice areas include the following:

Customizable Billing Structures

Every practice area has its own way of handling fees. A family law attorney working on a divorce case might bill by the hour, while a personal injury lawyer works on contingency. Some firms also use blended billing, charging different rates for partners, associates, and paralegals. Good legal time tracking software can (and should) provide settings that accommodate any billing structure you use.

Mobile Access

If you’re in a practice area that takes you away from the office often, it’s great to have a way to record billable hours while you’re on the move. The best time tracking software will come with a mobile time and billing app that you can run on any smart device, so you don’t miss a minute of work you put in.

Detailed Reporting

No matter how a firm bills, reporting features provide valuable insights into time management, case progress, and profitability. Running reports on pending invoices, total hours worked per case, or time spent on specific tasks can help firms identify inefficiencies and adjust workloads accordingly.

For firms that bill hourly, reports can highlight unbilled time and compare billable targets to actual hours worked. Those handling flat-fee matters can track how much time is spent on each case type to assess whether their pricing is truly profitable. Contingency firms can analyze case timelines to better estimate how long similar cases will take in the future.

Auto-Text Abbreviations

Clear and consistent billing makes invoices easier for clients to understand and reduces the chances of disputes. Auto-text shortcuts help attorneys in any practice area log time faster by filling in commonly used descriptions with just a few keystrokes. Instead of typing out “Reviewed and responded to client email regarding…” every time, an attorney can use a preset abbreviation, like “RR,” to generate the first part of the entry instantly. Over time, these small efficiencies add up, making billing faster and more accurate across the board.

As a final note, time tracking software works best when it’s part of a complete legal practice management software. This cuts down on the amount of software you need to manage your billing and invoicing process, making the entire process simpler and more accurate.

What Is the Tool for Tracking Billable Hours for Free?

Truthfully, there aren’t any free tools that track billable hours — at least, not any that were designed for it. You could possibly try using free tools like Google Sheets or other open-source platforms, but ultimately, they won’t have enough function to be worth your time (literally).

Quality time tracking software costs money because it’s maintained by service providers who not only keep your data secure but also help you maximize the software’s potential. Even if there is time tracking software that’s free to use, you should proceed with caution. Some providers try to lure you in with a “freemium” option, which sounds like a good idea until you see why it’s free.

Free-to-use time tracking software typically is lacking in one or more areas: security, function, usability, customer support, you name it. And if it is usable, it will likely come with heavy restrictions designed to frustrate you into purchasing the full, paid version. So, really, it’s just a ploy to hook you in and get you to spend money.

Using time tracking software should create processes that are better than doing it by hand, “better” meaning faster, more efficient, more accurate, and ultimately more profitable. Free software is free for a reason, and paying for software is not a downside; in fact, with the right time tracking software, you can capture more billable time, reduce errors, and spend less time on administrative work — ultimately increasing revenue.

What Percentage of Lawyers’ Hours Are Billable with Software vs. Without?

On average, about a third of the hours lawyers work (30%) qualify as billable hours. This may seem like a small number if you’re not an attorney, but lawyers know firsthand how much time they spend on non-billable work, from business development to tedious admin tasks. Thankfully, there is a way lawyers can improve that percentage right away: by using time tracking software.

Time tracking software makes tracking billable hours easier, quicker, and more efficient. It also leads to a far more accurate representation of your day-to-day workflow as an attorney. Tracking in real-time helps reduce forgotten entries, and small increments of work are easier to capture; even a quick email to a client that takes five minutes can quickly be recorded. Plus, with software formulas calculating the final invoice based on your hourly rates, there is much less room for error.

Using time tracking software also saves you time on billing and invoicing. You can set up automated workflows for the most repetitive, rote tasks that go into your job — for example, the steps you go through for client intake, or the different workflows for different types of cases. With less time spent on repetitive work, you can spend more time connecting with your clients. And with a written record of the tasks you accomplish for each case, it’s much easier to make sure you didn’t miss anything when you’re drafting the invoice.

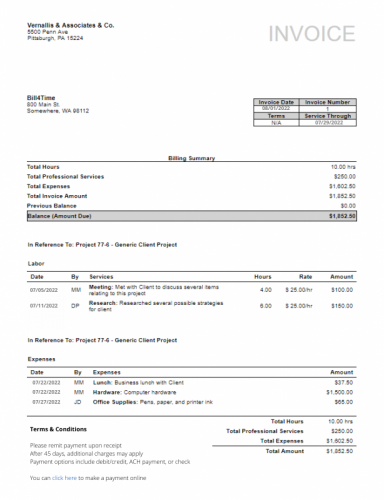

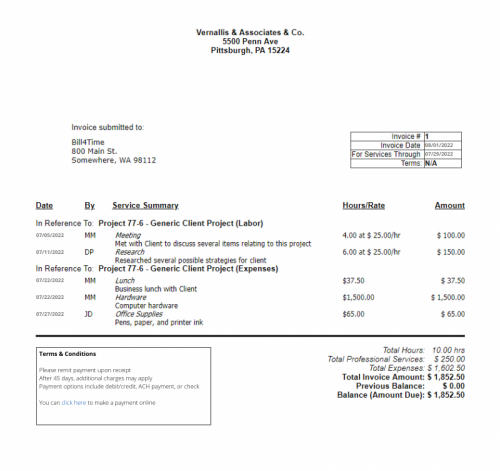

Bill4Time: The Ultimate Attorney Billing Cheat Sheet

Are you tired of manually adding up billable hours in a spreadsheet, asking yourself, “How many billable hours is 45 minutes?” yet again? If so, maybe it’s time for Bill4Time to help you out. This software is the most efficient way to track billable hours, especially because time tracking is only one part of Bill4Time’s complete practice management solution. You can capture your entire workflow in one place, eliminating several points of transferring data and cutting down on potential billing errors.

We welcome you to try Bill4Time yourself and see how much it can help your practice. Sign up for a free trial today, or click the button below to schedule a free demo. We look forward to helping you save effort, time, and money in your practice!